tt

tt

tt

tt

tt

tt

Civilization

•

Shipyards, Graveyards

In 2024, one Chinese company built more commercial vessels by tonnage than the United States has produced since the end of World War II.

Get the Mag in Print.

Arena publishes four stunning print editions per year, full of stories just like this one on American technology, capital, and industry.

Most stories about American industrialism have turned from inspirational myths into cautionary tales. One such story is that of the New York Shipbuilding Corporation in Camden, New Jersey. Founded in 1899, New York Ship grew to become the largest shipyard in the world by 1917. World War I sparked such a shipbuilding boom that the War Department had to fund a new city — Yorkship Village — just to house the labor force for New York Ship; it was the first federally funded planned community.

By the Second World War, New York Ship employed 47,000 across a 160-acre site along two miles of the Delaware River. What started as a factory had become an entire economy built to power the largest and most productive shipyard on Earth. New York Ship delivered 670 merchant and naval ships during its life, including three nuclear submarines and even the first nuclear-powered merchant ship.

By the end of WWII, America’s fleet represented 50,000,000 deadweight tons — a measure of total carrying capacity — two-thirds of global tonnage. But after the war ended, the burden of upkeep for such a large fleet felt unnecessary, leading the US to immediately start mothballing and scrapping ships rather than maintaining them. The Cold War sustained demand for specialized naval work, like nuclear submarines and carriers, but that work concentrated in a select group of dedicated yards. Meanwhile, commercial shipbuilding migrated to lower-cost foreign yards. Caught between a shrinking commercial market and increasingly specialized naval contracts, New York Ship didn’t have the business to stay afloat. By 1968, it had shut its doors. Camden, the city that powered New York Ship, tracks an eerie road map for what happens when industrialism falters. The city lost a third of its population, including 30,000 manufacturing jobs. It now faces a poverty rate of 28.5% and has become one of the most dangerous cities in the country.

The New York Shipbuilding Corporation is just one of dozens of examples of the cost of assuming that America no longer needed a strong industrial base. Particularly in the 1980s, the US came to the conclusion that manufacturing and shipbuilding were commodity processes better suited for lower-cost labor markets in Asia. We’ve seen the same dynamic play out in semiconductors, batteries, mining, and pharmaceuticals. But shipbuilding represents a distinctly gnarly systems problem tangled between defense funding, policy, and a fading American manufacturing core.

Why Build Ships?

Any national soul-searching about reindustrialization must start by disabusing ourselves of the notion that we don’t really need to build our own ships. We do. For most Americans, boats are a leisure category — a pleasure cruise, a fishing trip — while the working ocean has faded from the national imagination in a way that airports and interstates haven’t. While airplanes and highways may feel like the global connective tissue, the reality is that 80% of trade volume moves by sea. Without domestic shipbuilding capacity, the flow of global trade, including energy, raw materials, and consumer goods, is ultimately at the mercy of those who do control it.

The last few years have given us countless examples of that vulnerability. COVID pushed the median cost of transporting a shipping container from $2,000 to $20,000. When the Ever Given, a massive container ship, blocked the Suez Canal in March 2021 for six days, each day of disruption held up over $9 billion worth of goods. And when the recent US-Israeli strikes on Iran led Iran to effectively halt shipping through the Strait of Hormuz, it cut off 20 million barrels of oil per day, representing roughly 20% of global seaborne oil volumes.

Alfred Thayer Mahan, a Navy officer and historian described as “an apostle of sea power,” famously argued that “whoever rules the waves rules the world.” He saw the need for a navy as springing from the existence of peaceful commercial shipping. Increasingly, we live in a world where “peaceful commercial shipping” is more at risk than it has been in decades, owing to the volatility surrounding global chokepoints like Hormuz and the Taiwan Strait. The Council on Foreign Relations has put the odds of “a cross-strait crisis between China and Taiwan” at 50% in 2026. Such a crisis could dwarf a Hormuz closure in its ramifications for the global economy; nearly half of the world’s container shipping passes through the Taiwan Strait each year.

The seafaring domain is critical. The threat of great power conflict draws closer; a conflict between the US and China that may define the 21st century; a US-China war over Taiwan could deliver a roughly $10 trillion shock to the global economy in its first year, nearly 10% of global GDP — larger than COVID, the 2008 financial crisis, or the war in Ukraine. The US itself would absorb a 6 to 7% GDP hit, primarily through severed access to advanced semiconductors and the collapse of shipping through one of the world’s busiest sea lanes. Unfortunately, the majority of the ocean-going vessels are built by our would-be competitor.

In 2024 alone, one Chinese company built more commercial vessels by tonnage than the United States has produced since the end of World War II. Today, the US accounts for roughly 0.1% of the global commercial shipbuilding market while China accounts for 53%, up from just under 10% in 2000. China has become the dominant global shipbuilding superpower. It builds the vast majority of global shipping, including shipping critical to US naval power. Three of the ten oil tankers in the US fleet designed to carry fuel for military operations were constructed in Chinese yards. Seven of the twelve ships in the Maritime Security Fleet are made in China. The dependence is reckless, but the economic justification is straightforward: Regulators only require these ships to be US-flagged and crewed; otherwise, the ships would cost roughly $200 million, instead of their current sticker price of $50 million.

Meanwhile, domestically, US shipyards are failing to deliver on Navy shipbuilding goals. Some projects, like the Virginia-class submarine program, running at just 60% of its target production rate, with some ships delayed by as much as three years. Going forward, the US Naval fleet is already 20% short of the minimum capacity needed to carry out core missions. And that shortfall will continue to grow as maintenance backlogs pile up.

Meanwhile, the Chinese Navy, which surpassed the US Navy in total fleet size around 2020, keeps extending its lead. Huntington Ingalls Industries, the US defense prime most focused on seafaring, reported a backlog of $56.9 billion in 2025 — roughly five-years of work at current production rates. Even if Congress tripled shipbuilding appropriations tomorrow, Huntington Ingalls couldn’t build meaningfully faster. China’s advanced capacity, meanwhile, enabled it to add 30 ships to its fleet last year, while the US decommissioned 19 ships and built six, for a net loss of 13. In a protracted naval conflict, China can replace what it loses. We cannot.

To address this vulnerability, we must resurrect our national shipbuilding industry. But any attempt to do so must reckon with the chicken-and-egg problems inherent in bootstrapping a dying industry back into global competitiveness.

Shipbuilding’s Doom Loop

Every industrial process is a system; each input has process and timing dependencies, and every output demands execution. But when the process includes dozens of states and countries, multiple regulatory bodies across land and sea, and thousands of suppliers, each with their own regulatory regime and manufacturing idiosyncrasies, that system becomes almost hopelessly complex.

Regaining domestic shipbuilding capacity in the US means reckoning with a doom loop of interdependencies: labor, stable demand, competitive costs, scale, supply chain depth, and functional shipyards.

You can’t attract workers without stable demand: Shipbuilding apprenticeship completion rates sit below 35%. Even major shipyards, like Puget Sound, only begin with around 200 apprentices. The US Merchant Marine Academy, which offers a Marine Engineering and Shipyard Management major, was described by Transportation Secretary Sean Duffy as “dilapidated”. For those who make it into the shipbuilding industry, first-year attrition runs around 50-60% even at the most consistent shipyards. This attrition happens because there is no confidence in demand signals relative to more reliable industries, like oil and gas or construction. What’s more, around 27% of maritime workers are over the age of 55, meaning we’ll see a silver tsunami of retirements over the next decade.

You can’t generate stable demand without competitive costs: Asian shipyards produce at 5-6x lower prices and twice the delivery speed, driven in part by the massive regulatory burden American shipyards carry. Every input in the US, from labor to steel, is dramatically more expensive. No rational commercial buyer will pay that premium unless compelled by law or subsidy. Even artificial demand from the US government has wavered, with multi-billion-dollar shipbuilding contracts fluctuating between administrations.

You can’t achieve competitive costs without scale: China builds 1,000 commercial ships per year compared to about 10 in the US. Everything gets cheaper with scale. Workers move down learning curves faster with repetition, suppliers price lower with volume, and large workforces can specialize instead of generalize. As a result, the fixed costs of running a shipyard — the cranes, docks, management, financing — spread across more ships, making each one cheaper.

You can’t achieve scale without supply chain depth: Even a simple commercial ship requires thousands of components from hundreds of suppliers. Since 2000, the US has lost more than 25,000 of those suppliers. Some components, like marine diesel engines or marine-grade steel, have limited or no domestic production left. Of the six American companies manufacturing large marine diesel engines before 1980, only one — Fairbanks Morse Defense — still exists, surviving exclusively off of military contracts. Suppliers have done the math and found the US market wanting. No one will invest in marine diesel engine production for a market of ~10 ships per year.

You can’t achieve supply chain depth without functional shipyards: Of all the bottlenecks, shipyards themselves may be the hardest to resolve. You need deepwater coastal sites — exactly the kind of sites that attract the most onerous regulation — including 50-100+ contiguous acres of waterfront with deep draft access, heavy industrial zoning, and proximity to rail or highway. There are vanishingly few sites in the US that meet all those criteria and aren’t already developed.

Which brings us back to labor: Even if you could build a functional shipyard, with access to a deep supply chain, commanding sizable demand at competitive prices, you still need workers to staff it. Which brings us full circle.

No matter which lever you pull, nothing makes enough of a difference on its own. Legislation can artificially lift demand, but it cannot sustain a workforce. Foreign expertise can bridge some of the knowledge gap, but it can’t magically spin up a supplier base. What’s more, solving all of these issues simultaneously requires a level of sustained, coordinated, multi-decade industrial policy that the US hasn’t demonstrated since before the Cold War.

The solution here isn’t akin to the CHIPS Act for semiconductors or the IRA for batteries, solutions that were, primarily, acts of capital deployment by the federal government. The closest analogy for a solution is the interstate highway system. From 1956 to the 1980s, the National Interstate and Defense Highways Act enacted a 20+ year, multi-administration, federally funded infrastructure program that required simultaneous land acquisition, engineering, workforce development, materials supply, and political consensus across all 50 states.

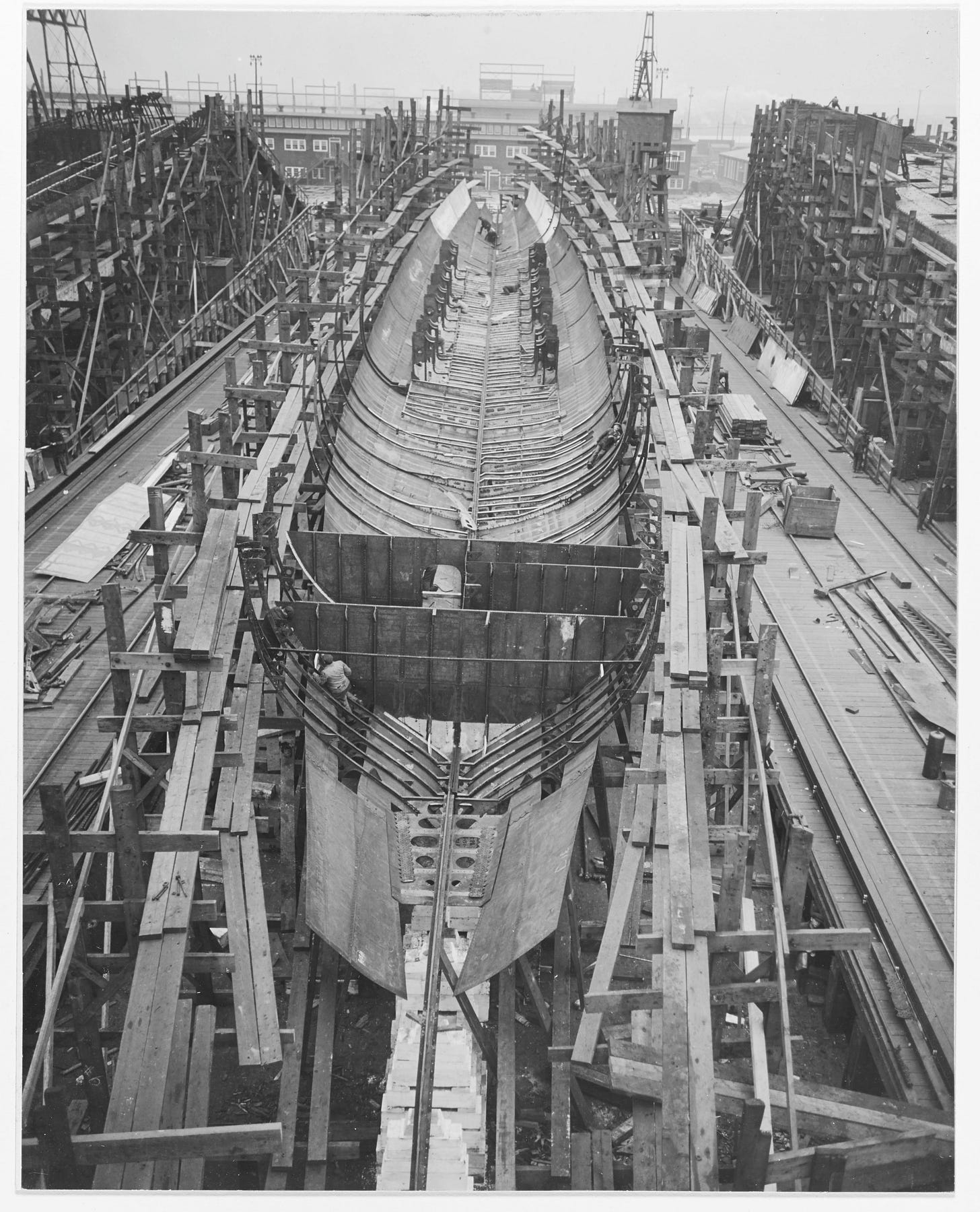

USS Sturtevant (DD-240) under construction at New York Shipbuilding Corporation on December 1, 1918. Credit: Naval History and Heritage Command, Washington, DC

Some good news and some bad news there.

The good news is Washington seems committed to prioritizing shipbuilding, at least for now. Congress has consistently appropriated $2.5 billion more per year for shipbuilding than the Navy has requested since 2015. In 2025, Congress dedicated $34 billion to shipbuilding through the “Big Beautiful Bill,” making it the largest defense line item in a $150 billion Department of Defense budget. By placing shipbuilding at the top of the list of defense modernization priorities, Washington is signaling to private capital, allied industry, and the workforce that the sector has durable political backing.

The bad news is we don’t have 20 years to shore up America’s shipbuilding capacity, and it’s going to cost a lot more than $34 billion. What’s needed is an entirely new strategy. In World War II, we leveraged commercial industrial dominance to build the Arsenal of Democracy. But today, we have a dramatically limited ability to transition our domestic industry into wartime production because we don’t have a domestic industry to transition. We can’t run back the same playbook. Things have changed.

New Problems Need New Playbooks

In World War II, the US simply outbuilt our enemies. William S. Knudsen described the strategy as “[smothering] the enemy in an avalanche of production, the likes of which [they] had never seen, nor dreamed possible.” That won’t work this time because, today, China occupies the dominant manufacturing position the US held in 1942. Where the US produced around 40% of global manufacturing output in 1942, China represents 35% today. In fact, China has even more unilateral capability than WWII-era America did given its authoritarian political and economic system, including heavily subsidized financing and “military-civil fusion,” which funnels commercial capacity directly into naval output.

Instead, we must rely on innovation rather than sheer output. Trying to beat China at its own game of sheer production volume would be misguided. The opportunity lies in finding the highest leverage innovation. There is actually a precedent for this from World War II: The Liberty Ship program popularized arc welding, which is running an electric current to fuse steel plates into a continuous seam, to replace riveting, which required skilled teams hammering heated pins through pre-drilled holes. That enabled rapid prefabricated shipbuilding with minimal training required. That one innovation took construction of each ship from 355 days down to 40 — within months. These wartime welding advances in shipbuilding contributed to broader US manufacturing efficiencies post-war.

The focus should be on what could allow us to leapfrog ahead, not just catch up. Modular construction techniques would allow components to be built in distributed locations and assembled more efficiently, prioritizing building many standardized, cost-effective vessels over a few overengineered ones. Integrated autonomous systems and AI-driven production software could multiply the impact of both.

Jumping ahead will also require meaningful acceleration of digital integration. Unfortunately, we’re not currently moving in the right direction on this front. The Navy has hollowed out its in-house technical capacity, having cut the number of naval architects and engineers from 1,200 to 300 since the 1990s; a post-Cold War cost-saving measure that transferred design work to private industry just as private industry itself began to atrophy. As a result, we’re seeing costly design flaws and mid-construction rework across major programs, driving up costs by at least 25%.

Closing that gap doesn’t require inventing new technology; just deploying what already exists. Advanced block assembly, robotic welding, and AI-driven logistics can halve construction timelines. The Navy’s new Shipbuilding Operating System (Ship OS) — a $448 million Palantir-built platform launched in December 2025 — integrates planning software, legacy records, and operational sensor inputs to flag bottlenecks, optimize workflows, and refine risk models. Similar tools at General Dynamics Electric Boat cut planning tasks from over 160 hours to under 10 minutes. At Portsmouth Naval Shipyard, Ship OS AI systems have cut material review times from weeks to hours. Those are the kinds of leverage points that could be replicated across the industry to enable the US to work smarter, rather than harder.

The goal would be to shift the economic curve of shipbuilding in our favor. A comparable analog is visible in the space industry. We were able to shift from a government-dependent monopoly with high, administered prices to a thriving, competitive ecosystem after SpaceX demonstrated reliable reusable rockets that dramatically reduced launch costs. In shipbuilding, modular construction and software-driven production automation can play a similar catalytic role in which high-integrity blocks, standardized interfaces, and tightly sequenced assembly can reduce labor hours per ton, shorten cycle times, and lowering barriers for new entrants in the space.

While we’ve made progress on some of the most compelling innovations, we’re far from the cutting edge. In fact, some of the best testing grounds are in allied nations like South Korea, with companies like HD Hyundai leading the charge in smart manufacturing, robotic welding, and digital twin systems. If innovation is where we’re going to pull ahead, we aren’t going to be able to do it alone.

Walking (With Allies) Before We Can Run

We can’t lose sight of the long-term vision of rebuilding domestic shipbuilding capacity in the US. Focusing on innovation over raw output is critical. But in the short-term, we’ll have to alleviate some of our dependencies by leaning even more heavily on another: international partnerships.

It’s worth noting that many of the most important processes in modern shipbuilding were developed in the US during the 1950s and then exported to Japan for execution. Advances like statistical process control, a method for using real-time measurement to catch manufacturing defects as they emerge, rather than inspecting finished products, were invented by Walter Shewhart at Bell Labs, then brought to Japan by W. Edwards Deming, who over the course of two decades, trained almost 15,000 Japanese engineers in them. Over time, those capabilities spread to other allies, like South Korea — and eventually to China.

Competing with Chinese capacity can feel insurmountable when you compare its 53% of global capacity to our 0.1%. But the playing field feels dramatically more even when compared to the combined share of Japan and South Korea at around 43%. That capacity has enabled those allied nations to retain the scale, skilled labor, and industrial depth the United States has lost. We’re already seeing a precedent for this kind of allied collaboration in semiconductors, with TSMC’s $65 billion investment into its Arizona facilities, the largest single foreign direct investment in US history.

And a shipbuilding partnership is a win-win for a country like South Korea. Despite a half-century of continuous large-scale shipbuilding, it still faces labor shortages and relies on foreign nationals for roughly a quarter of its shipyard workforce. Sooner or later, every nation will require rapid innovation and, given the US’s industrial deficiencies, a collaborative approach would be more effective than going it alone. Allied countries like Japan and South Korea can provide the stop-gap of workforce expertise and capital required, but in the long run everyone stands to benefit from an independent American shipbuilding innovation machine.

The critical distinction in relying on allies today, compared to the offshoring of the late 20th century, is about capability flows. In the 1980s, America surrendered the technological and workforce capabilities around shipbuilding, allowing them to flow towards other countries. Today’s proposed partnerships invert that flow. American workers travel to South Korea to absorb labor capabilities that then return home; Korean capital and equipment flow into American shipyards to rebuild industrial infrastructure on US soil. The long-term question is whether we can treat this as a generational capability build rather than a cost-minimization play.

Precious Few Sites

Beyond labor and supply chains, the US faces a hard physical constraint: space. The US has roughly 150 private shipyards, but only seven can build major oceangoing vessels, and those seven are dwarfed by Jiangnan Shipyard alone, a single Chinese yard that has more capacity than all US shipyards combined. China also manufactures roughly 80% of ship-to-shore cranes and 96% of shipping containers used in the US. Since the 1950s, the number of American shipyards capable of constructing large oceangoing vessels has declined by more than 80%. The Brooklyn Navy Yard shut in 1966. The Philadelphia Naval Shipyard shut in 1996. The Mare Island yard outside San Francisco shut in 1993. Each of these was, at one point, among the most productive shipbuilding facilities in the world. Their workforces have long since retired. Even if the appetite for additional shipyards grows, there is simply a limited number of viable sites for large-scale shipyard construction.

Modular construction could alleviate that barrier. By splitting a vessel into discrete block sections that inland or distributed facilities can build in parallel, the US can leverage interior regions previously considered irrelevant to the industry. Completed modular sections would then be shipped to coastal yards for final assembly. The Navy has already expressed support for this approach. Modular construction could double the current annual production rate of existing US shipyards and grow employment in the sector from roughly 400,000 to nearly one million.

Our Future Is Just 30 Miles Downriver From Our Past

Just 30 miles down the Delaware River from the New York Shipbuilding Corporation’s former yards lies a symbol of the future of American shipbuilding. The Philly Shipyard, recently renamed Hanwha Philly Shipyard, is where South Korea is making a $5 billion investment to execute exactly the playbook we’re describing. An all-out ally-first innovation build-out.

Starting with labor, Hanwha is already sending American workers to Korea for training, while simultaneously embedding Korean production systems into its operations in Philadelphia. It has implemented a joint-build model with South Korea for an LNG carrier ordered at their Philly Shipyard — a project that combines Korean engineers, production systems, and supply-chain processes with the US workforce, allowing American employees to gain hands-on exposure to advanced construction techniques, regaining the process knowledge the shipbuilding industry spent decades losing.

The $34 billion American investment in shipbuilding is the down payment. The Hanwha partnership is a bridge loan. Modular construction and software-driven production are the long-term bets. But none of it works without the one thing the US has failed to sustain for the last 40 years: the political will to treat shipbuilding as a generational commitment, not a line item. The Delaware River, running from the ghost of New York Ship’s past to Philly’s rebirth, is where we find out whether the country still has the resolve to build.

Civilization

•

Shipyards, Graveyards

In 2024, one Chinese company built more commercial vessels by tonnage than the United States has produced since the end of World War II.

Get the Mag in Print.

Arena publishes four stunning print editions per year, full of stories just like this one on American technology, capital, and industry.

Most stories about American industrialism have turned from inspirational myths into cautionary tales. One such story is that of the New York Shipbuilding Corporation in Camden, New Jersey. Founded in 1899, New York Ship grew to become the largest shipyard in the world by 1917. World War I sparked such a shipbuilding boom that the War Department had to fund a new city — Yorkship Village — just to house the labor force for New York Ship; it was the first federally funded planned community.

By the Second World War, New York Ship employed 47,000 across a 160-acre site along two miles of the Delaware River. What started as a factory had become an entire economy built to power the largest and most productive shipyard on Earth. New York Ship delivered 670 merchant and naval ships during its life, including three nuclear submarines and even the first nuclear-powered merchant ship.

By the end of WWII, America’s fleet represented 50,000,000 deadweight tons — a measure of total carrying capacity — two-thirds of global tonnage. But after the war ended, the burden of upkeep for such a large fleet felt unnecessary, leading the US to immediately start mothballing and scrapping ships rather than maintaining them. The Cold War sustained demand for specialized naval work, like nuclear submarines and carriers, but that work concentrated in a select group of dedicated yards. Meanwhile, commercial shipbuilding migrated to lower-cost foreign yards. Caught between a shrinking commercial market and increasingly specialized naval contracts, New York Ship didn’t have the business to stay afloat. By 1968, it had shut its doors. Camden, the city that powered New York Ship, tracks an eerie road map for what happens when industrialism falters. The city lost a third of its population, including 30,000 manufacturing jobs. It now faces a poverty rate of 28.5% and has become one of the most dangerous cities in the country.

The New York Shipbuilding Corporation is just one of dozens of examples of the cost of assuming that America no longer needed a strong industrial base. Particularly in the 1980s, the US came to the conclusion that manufacturing and shipbuilding were commodity processes better suited for lower-cost labor markets in Asia. We’ve seen the same dynamic play out in semiconductors, batteries, mining, and pharmaceuticals. But shipbuilding represents a distinctly gnarly systems problem tangled between defense funding, policy, and a fading American manufacturing core.

Why Build Ships?

Any national soul-searching about reindustrialization must start by disabusing ourselves of the notion that we don’t really need to build our own ships. We do. For most Americans, boats are a leisure category — a pleasure cruise, a fishing trip — while the working ocean has faded from the national imagination in a way that airports and interstates haven’t. While airplanes and highways may feel like the global connective tissue, the reality is that 80% of trade volume moves by sea. Without domestic shipbuilding capacity, the flow of global trade, including energy, raw materials, and consumer goods, is ultimately at the mercy of those who do control it.

The last few years have given us countless examples of that vulnerability. COVID pushed the median cost of transporting a shipping container from $2,000 to $20,000. When the Ever Given, a massive container ship, blocked the Suez Canal in March 2021 for six days, each day of disruption held up over $9 billion worth of goods. And when the recent US-Israeli strikes on Iran led Iran to effectively halt shipping through the Strait of Hormuz, it cut off 20 million barrels of oil per day, representing roughly 20% of global seaborne oil volumes.

Alfred Thayer Mahan, a Navy officer and historian described as “an apostle of sea power,” famously argued that “whoever rules the waves rules the world.” He saw the need for a navy as springing from the existence of peaceful commercial shipping. Increasingly, we live in a world where “peaceful commercial shipping” is more at risk than it has been in decades, owing to the volatility surrounding global chokepoints like Hormuz and the Taiwan Strait. The Council on Foreign Relations has put the odds of “a cross-strait crisis between China and Taiwan” at 50% in 2026. Such a crisis could dwarf a Hormuz closure in its ramifications for the global economy; nearly half of the world’s container shipping passes through the Taiwan Strait each year.

The seafaring domain is critical. The threat of great power conflict draws closer; a conflict between the US and China that may define the 21st century; a US-China war over Taiwan could deliver a roughly $10 trillion shock to the global economy in its first year, nearly 10% of global GDP — larger than COVID, the 2008 financial crisis, or the war in Ukraine. The US itself would absorb a 6 to 7% GDP hit, primarily through severed access to advanced semiconductors and the collapse of shipping through one of the world’s busiest sea lanes. Unfortunately, the majority of the ocean-going vessels are built by our would-be competitor.

In 2024 alone, one Chinese company built more commercial vessels by tonnage than the United States has produced since the end of World War II. Today, the US accounts for roughly 0.1% of the global commercial shipbuilding market while China accounts for 53%, up from just under 10% in 2000. China has become the dominant global shipbuilding superpower. It builds the vast majority of global shipping, including shipping critical to US naval power. Three of the ten oil tankers in the US fleet designed to carry fuel for military operations were constructed in Chinese yards. Seven of the twelve ships in the Maritime Security Fleet are made in China. The dependence is reckless, but the economic justification is straightforward: Regulators only require these ships to be US-flagged and crewed; otherwise, the ships would cost roughly $200 million, instead of their current sticker price of $50 million.

Meanwhile, domestically, US shipyards are failing to deliver on Navy shipbuilding goals. Some projects, like the Virginia-class submarine program, running at just 60% of its target production rate, with some ships delayed by as much as three years. Going forward, the US Naval fleet is already 20% short of the minimum capacity needed to carry out core missions. And that shortfall will continue to grow as maintenance backlogs pile up.

Meanwhile, the Chinese Navy, which surpassed the US Navy in total fleet size around 2020, keeps extending its lead. Huntington Ingalls Industries, the US defense prime most focused on seafaring, reported a backlog of $56.9 billion in 2025 — roughly five-years of work at current production rates. Even if Congress tripled shipbuilding appropriations tomorrow, Huntington Ingalls couldn’t build meaningfully faster. China’s advanced capacity, meanwhile, enabled it to add 30 ships to its fleet last year, while the US decommissioned 19 ships and built six, for a net loss of 13. In a protracted naval conflict, China can replace what it loses. We cannot.

To address this vulnerability, we must resurrect our national shipbuilding industry. But any attempt to do so must reckon with the chicken-and-egg problems inherent in bootstrapping a dying industry back into global competitiveness.

Shipbuilding’s Doom Loop

Every industrial process is a system; each input has process and timing dependencies, and every output demands execution. But when the process includes dozens of states and countries, multiple regulatory bodies across land and sea, and thousands of suppliers, each with their own regulatory regime and manufacturing idiosyncrasies, that system becomes almost hopelessly complex.

Regaining domestic shipbuilding capacity in the US means reckoning with a doom loop of interdependencies: labor, stable demand, competitive costs, scale, supply chain depth, and functional shipyards.

You can’t attract workers without stable demand: Shipbuilding apprenticeship completion rates sit below 35%. Even major shipyards, like Puget Sound, only begin with around 200 apprentices. The US Merchant Marine Academy, which offers a Marine Engineering and Shipyard Management major, was described by Transportation Secretary Sean Duffy as “dilapidated”. For those who make it into the shipbuilding industry, first-year attrition runs around 50-60% even at the most consistent shipyards. This attrition happens because there is no confidence in demand signals relative to more reliable industries, like oil and gas or construction. What’s more, around 27% of maritime workers are over the age of 55, meaning we’ll see a silver tsunami of retirements over the next decade.

You can’t generate stable demand without competitive costs: Asian shipyards produce at 5-6x lower prices and twice the delivery speed, driven in part by the massive regulatory burden American shipyards carry. Every input in the US, from labor to steel, is dramatically more expensive. No rational commercial buyer will pay that premium unless compelled by law or subsidy. Even artificial demand from the US government has wavered, with multi-billion-dollar shipbuilding contracts fluctuating between administrations.

You can’t achieve competitive costs without scale: China builds 1,000 commercial ships per year compared to about 10 in the US. Everything gets cheaper with scale. Workers move down learning curves faster with repetition, suppliers price lower with volume, and large workforces can specialize instead of generalize. As a result, the fixed costs of running a shipyard — the cranes, docks, management, financing — spread across more ships, making each one cheaper.

You can’t achieve scale without supply chain depth: Even a simple commercial ship requires thousands of components from hundreds of suppliers. Since 2000, the US has lost more than 25,000 of those suppliers. Some components, like marine diesel engines or marine-grade steel, have limited or no domestic production left. Of the six American companies manufacturing large marine diesel engines before 1980, only one — Fairbanks Morse Defense — still exists, surviving exclusively off of military contracts. Suppliers have done the math and found the US market wanting. No one will invest in marine diesel engine production for a market of ~10 ships per year.

You can’t achieve supply chain depth without functional shipyards: Of all the bottlenecks, shipyards themselves may be the hardest to resolve. You need deepwater coastal sites — exactly the kind of sites that attract the most onerous regulation — including 50-100+ contiguous acres of waterfront with deep draft access, heavy industrial zoning, and proximity to rail or highway. There are vanishingly few sites in the US that meet all those criteria and aren’t already developed.

Which brings us back to labor: Even if you could build a functional shipyard, with access to a deep supply chain, commanding sizable demand at competitive prices, you still need workers to staff it. Which brings us full circle.

No matter which lever you pull, nothing makes enough of a difference on its own. Legislation can artificially lift demand, but it cannot sustain a workforce. Foreign expertise can bridge some of the knowledge gap, but it can’t magically spin up a supplier base. What’s more, solving all of these issues simultaneously requires a level of sustained, coordinated, multi-decade industrial policy that the US hasn’t demonstrated since before the Cold War.

The solution here isn’t akin to the CHIPS Act for semiconductors or the IRA for batteries, solutions that were, primarily, acts of capital deployment by the federal government. The closest analogy for a solution is the interstate highway system. From 1956 to the 1980s, the National Interstate and Defense Highways Act enacted a 20+ year, multi-administration, federally funded infrastructure program that required simultaneous land acquisition, engineering, workforce development, materials supply, and political consensus across all 50 states.

USS Sturtevant (DD-240) under construction at New York Shipbuilding Corporation on December 1, 1918. Credit: Naval History and Heritage Command, Washington, DC

Some good news and some bad news there.

The good news is Washington seems committed to prioritizing shipbuilding, at least for now. Congress has consistently appropriated $2.5 billion more per year for shipbuilding than the Navy has requested since 2015. In 2025, Congress dedicated $34 billion to shipbuilding through the “Big Beautiful Bill,” making it the largest defense line item in a $150 billion Department of Defense budget. By placing shipbuilding at the top of the list of defense modernization priorities, Washington is signaling to private capital, allied industry, and the workforce that the sector has durable political backing.

The bad news is we don’t have 20 years to shore up America’s shipbuilding capacity, and it’s going to cost a lot more than $34 billion. What’s needed is an entirely new strategy. In World War II, we leveraged commercial industrial dominance to build the Arsenal of Democracy. But today, we have a dramatically limited ability to transition our domestic industry into wartime production because we don’t have a domestic industry to transition. We can’t run back the same playbook. Things have changed.

New Problems Need New Playbooks

In World War II, the US simply outbuilt our enemies. William S. Knudsen described the strategy as “[smothering] the enemy in an avalanche of production, the likes of which [they] had never seen, nor dreamed possible.” That won’t work this time because, today, China occupies the dominant manufacturing position the US held in 1942. Where the US produced around 40% of global manufacturing output in 1942, China represents 35% today. In fact, China has even more unilateral capability than WWII-era America did given its authoritarian political and economic system, including heavily subsidized financing and “military-civil fusion,” which funnels commercial capacity directly into naval output.

Instead, we must rely on innovation rather than sheer output. Trying to beat China at its own game of sheer production volume would be misguided. The opportunity lies in finding the highest leverage innovation. There is actually a precedent for this from World War II: The Liberty Ship program popularized arc welding, which is running an electric current to fuse steel plates into a continuous seam, to replace riveting, which required skilled teams hammering heated pins through pre-drilled holes. That enabled rapid prefabricated shipbuilding with minimal training required. That one innovation took construction of each ship from 355 days down to 40 — within months. These wartime welding advances in shipbuilding contributed to broader US manufacturing efficiencies post-war.

The focus should be on what could allow us to leapfrog ahead, not just catch up. Modular construction techniques would allow components to be built in distributed locations and assembled more efficiently, prioritizing building many standardized, cost-effective vessels over a few overengineered ones. Integrated autonomous systems and AI-driven production software could multiply the impact of both.

Jumping ahead will also require meaningful acceleration of digital integration. Unfortunately, we’re not currently moving in the right direction on this front. The Navy has hollowed out its in-house technical capacity, having cut the number of naval architects and engineers from 1,200 to 300 since the 1990s; a post-Cold War cost-saving measure that transferred design work to private industry just as private industry itself began to atrophy. As a result, we’re seeing costly design flaws and mid-construction rework across major programs, driving up costs by at least 25%.

Closing that gap doesn’t require inventing new technology; just deploying what already exists. Advanced block assembly, robotic welding, and AI-driven logistics can halve construction timelines. The Navy’s new Shipbuilding Operating System (Ship OS) — a $448 million Palantir-built platform launched in December 2025 — integrates planning software, legacy records, and operational sensor inputs to flag bottlenecks, optimize workflows, and refine risk models. Similar tools at General Dynamics Electric Boat cut planning tasks from over 160 hours to under 10 minutes. At Portsmouth Naval Shipyard, Ship OS AI systems have cut material review times from weeks to hours. Those are the kinds of leverage points that could be replicated across the industry to enable the US to work smarter, rather than harder.

The goal would be to shift the economic curve of shipbuilding in our favor. A comparable analog is visible in the space industry. We were able to shift from a government-dependent monopoly with high, administered prices to a thriving, competitive ecosystem after SpaceX demonstrated reliable reusable rockets that dramatically reduced launch costs. In shipbuilding, modular construction and software-driven production automation can play a similar catalytic role in which high-integrity blocks, standardized interfaces, and tightly sequenced assembly can reduce labor hours per ton, shorten cycle times, and lowering barriers for new entrants in the space.

While we’ve made progress on some of the most compelling innovations, we’re far from the cutting edge. In fact, some of the best testing grounds are in allied nations like South Korea, with companies like HD Hyundai leading the charge in smart manufacturing, robotic welding, and digital twin systems. If innovation is where we’re going to pull ahead, we aren’t going to be able to do it alone.

Walking (With Allies) Before We Can Run

We can’t lose sight of the long-term vision of rebuilding domestic shipbuilding capacity in the US. Focusing on innovation over raw output is critical. But in the short-term, we’ll have to alleviate some of our dependencies by leaning even more heavily on another: international partnerships.

It’s worth noting that many of the most important processes in modern shipbuilding were developed in the US during the 1950s and then exported to Japan for execution. Advances like statistical process control, a method for using real-time measurement to catch manufacturing defects as they emerge, rather than inspecting finished products, were invented by Walter Shewhart at Bell Labs, then brought to Japan by W. Edwards Deming, who over the course of two decades, trained almost 15,000 Japanese engineers in them. Over time, those capabilities spread to other allies, like South Korea — and eventually to China.

Competing with Chinese capacity can feel insurmountable when you compare its 53% of global capacity to our 0.1%. But the playing field feels dramatically more even when compared to the combined share of Japan and South Korea at around 43%. That capacity has enabled those allied nations to retain the scale, skilled labor, and industrial depth the United States has lost. We’re already seeing a precedent for this kind of allied collaboration in semiconductors, with TSMC’s $65 billion investment into its Arizona facilities, the largest single foreign direct investment in US history.

And a shipbuilding partnership is a win-win for a country like South Korea. Despite a half-century of continuous large-scale shipbuilding, it still faces labor shortages and relies on foreign nationals for roughly a quarter of its shipyard workforce. Sooner or later, every nation will require rapid innovation and, given the US’s industrial deficiencies, a collaborative approach would be more effective than going it alone. Allied countries like Japan and South Korea can provide the stop-gap of workforce expertise and capital required, but in the long run everyone stands to benefit from an independent American shipbuilding innovation machine.

The critical distinction in relying on allies today, compared to the offshoring of the late 20th century, is about capability flows. In the 1980s, America surrendered the technological and workforce capabilities around shipbuilding, allowing them to flow towards other countries. Today’s proposed partnerships invert that flow. American workers travel to South Korea to absorb labor capabilities that then return home; Korean capital and equipment flow into American shipyards to rebuild industrial infrastructure on US soil. The long-term question is whether we can treat this as a generational capability build rather than a cost-minimization play.

Precious Few Sites

Beyond labor and supply chains, the US faces a hard physical constraint: space. The US has roughly 150 private shipyards, but only seven can build major oceangoing vessels, and those seven are dwarfed by Jiangnan Shipyard alone, a single Chinese yard that has more capacity than all US shipyards combined. China also manufactures roughly 80% of ship-to-shore cranes and 96% of shipping containers used in the US. Since the 1950s, the number of American shipyards capable of constructing large oceangoing vessels has declined by more than 80%. The Brooklyn Navy Yard shut in 1966. The Philadelphia Naval Shipyard shut in 1996. The Mare Island yard outside San Francisco shut in 1993. Each of these was, at one point, among the most productive shipbuilding facilities in the world. Their workforces have long since retired. Even if the appetite for additional shipyards grows, there is simply a limited number of viable sites for large-scale shipyard construction.

Modular construction could alleviate that barrier. By splitting a vessel into discrete block sections that inland or distributed facilities can build in parallel, the US can leverage interior regions previously considered irrelevant to the industry. Completed modular sections would then be shipped to coastal yards for final assembly. The Navy has already expressed support for this approach. Modular construction could double the current annual production rate of existing US shipyards and grow employment in the sector from roughly 400,000 to nearly one million.

Our Future Is Just 30 Miles Downriver From Our Past

Just 30 miles down the Delaware River from the New York Shipbuilding Corporation’s former yards lies a symbol of the future of American shipbuilding. The Philly Shipyard, recently renamed Hanwha Philly Shipyard, is where South Korea is making a $5 billion investment to execute exactly the playbook we’re describing. An all-out ally-first innovation build-out.

Starting with labor, Hanwha is already sending American workers to Korea for training, while simultaneously embedding Korean production systems into its operations in Philadelphia. It has implemented a joint-build model with South Korea for an LNG carrier ordered at their Philly Shipyard — a project that combines Korean engineers, production systems, and supply-chain processes with the US workforce, allowing American employees to gain hands-on exposure to advanced construction techniques, regaining the process knowledge the shipbuilding industry spent decades losing.

The $34 billion American investment in shipbuilding is the down payment. The Hanwha partnership is a bridge loan. Modular construction and software-driven production are the long-term bets. But none of it works without the one thing the US has failed to sustain for the last 40 years: the political will to treat shipbuilding as a generational commitment, not a line item. The Delaware River, running from the ghost of New York Ship’s past to Philly’s rebirth, is where we find out whether the country still has the resolve to build.

About the Author

Kyle Harrison is a General Partner at Contrary. Kyle founded Contrary Research in 2022 and leads Contrary’s investing efforts for companies from seed to scale. He previously worked at Index and Coatue, and has invested in companies like Anduril, Ramp, and Databricks. He is on X @kwharrison13.

• • •

Sawsan Haider is an Investment Analyst at Space VC. Previously a Senior Fellow at Contrary, she has an MS in Bioethics at Harvard Medical School. She has previously conducted AI alignment research at the University of Cambridge and was an analyst at Spring Venture Services.